Snapchat has recently released its performance update for Q4 2024, revealing an encouraging increase in user engagement and a revenue result that surpassed expectations. Nevertheless, the platform continues to face challenges as it navigates a crucial phase in its evolution and growth strategy.

In terms of user engagement, Snapchat has successfully added 10 million new daily active users in Q4, bringing the total to an impressive 453 million daily active users. This growth highlights Snapchat’s ability to attract and retain users, which is vital for its ongoing success in a competitive social media landscape.

Snapchat has demonstrated remarkable consistency with its user growth metrics. Over the last five quarters, the platform has averaged a steady addition of approximately 9 million extra users each quarter, showcasing its ability to maintain user interest and engagement.

Despite this positive trajectory, it is essential to recognize that Snapchat is growing without gaining significant momentum. Adding millions of users is undoubtedly a positive sign; however, the platform’s regional growth trends warrant closer examination within this broader context of expansion.

While Snap is experiencing user growth in the “Rest of World” category, it has faced a decline in American user numbers throughout the year, and growth in Europe has remained relatively stagnant, resulting in a flat trajectory. This disparity raises questions about Snapchat’s ability to penetrate developed markets where user engagement tends to be more lucrative.

These considerations become more pressing when you analyze critical financial metrics:

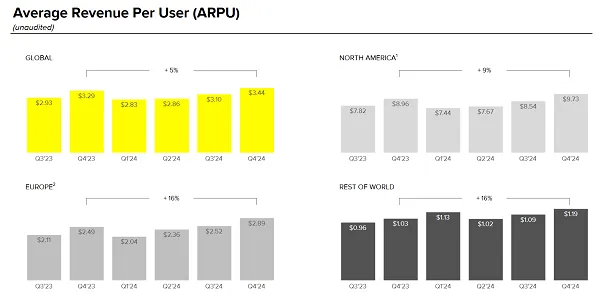

Snapchat continues to generate significantly higher revenue from its North American user base and users in more developed markets. Although growth in regions like Asia, particularly in India, is boosting Snap’s overall numbers, the absence of growth in higher-value regions undermines its financial potential.

While this situation offers a glimmer of hope for long-term potential, it raises concerns about Snapchat’s immediate outlook and its ability to capitalize on current trends.

Despite these challenges, Snapchat has managed to report profitability, achieving a 14% year-over-year revenue increase for the quarter, bringing in a total of $1.56 billion. This financial growth indicates that the platform is effectively leveraging its existing user base and advertising strategies.

Throughout the year, Snap generated an impressive $5.36 billion in revenue, reflecting a 16% year-over-year growth. This upward trajectory showcases the Snap team’s efforts to enhance its advertising offerings and seize opportunities in key markets. Notably, the company doubled its active advertiser count in the fourth quarter.

According to Snap:

“Direct Response ad revenue growth was up 14% year-over-year in Q4 and was the largest driver of our ad revenue growth in 2024. Strong demand for Pixel Purchase and App Purchase Optimizations led to revenue from app-based purchase optimizations growing more than 70% YoY in Q4.”

Snapchat is effectively capitalizing on the opportunities within its current framework while expanding its audience reach. This strategy has yielded results that exceed expectations; however, I remain cautious about Snap’s long-term expansion prospects, especially considering the limitations on ad display before reaching saturation.

On another positive note, Snap has reported that its Snapchat+ subscriber base has significantly increased from 7 million to 14 million in 2024, contributing an additional $500 million in annual revenue. This surge indicates that the promotional efforts around gifting Snapchat+ during the holiday season have proven effective, adding 2 million new subscribers during this period.

However, this achievement also highlights the challenges associated with subscription-based social media. Despite Snap’s success in attracting 14 million subscribers to its premium features, this revenue stream remains a fraction of the company’s overall income.

In contrast, Elon Musk’s ambitious goal to derive half of X’s revenue from subscriptions presents a daunting challenge. Currently, X Premium has around 1.3 million subscribers, underscoring the difficulties inherent in achieving such lofty targets.

Snapchat+ has emerged as a more successful initiative, providing users with a desirable package of add-ons that enhance their experience. Nevertheless, it remains a supplementary revenue source rather than a primary driver of income.

In terms of content engagement, Snap reported that more than a billion Snaps were shared publicly each month in Q4, marking a significant shift for a platform historically known for its private and enclosed user experience. This transformation reflects Snap’s efforts to encourage creators to share their content through monetization incentives, which likely contributed to the growth of its Spotlight feature, similar to TikTok’s video feed.

Increasing the availability of public content creates more opportunities for users to stay entertained and engaged within the app, making this a critical aspect of Snap’s ongoing strategy for growth.

Looking ahead, Snap has unveiled a revolutionary new generative AI model designed to produce high-resolution images directly on mobile devices in mere seconds. This technological advancement runs entirely on-device, significantly reducing the computational costs typically associated with larger, server-dependent models.

Snap expressed enthusiasm about integrating this technology into its platform in the coming months, aiming to enhance features such as AI Snaps and AI Bitmoji Backgrounds. By developing this in-house technology, Snap can offer its users fast and high-quality AI tools while minimizing operational costs.

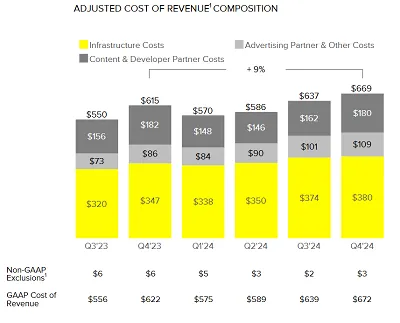

This initiative is particularly noteworthy given that Snap’s infrastructure costs continue to rise, highlighting the importance of cost-effective technological solutions.

Part of these rising costs is attributed to the ongoing development of its AR glasses, which are currently being tested with selected developers, paving the way for a future product launch.

Snap provided a sneak peek of its AR glasses last year, indicating that these devices are now in the hands of developers across the U.S. and several European countries, including Austria, France, Germany, Italy, Netherlands, and Spain.

Additionally, Snap recently announced a new initiative aimed at providing teachers and students with access to its AR glasses at a reduced cost, which could facilitate broader adoption of these innovative devices.

However, I have reservations about Snap’s ability to produce these glasses at a competitive price point without sacrificing quality in comparison to Meta’s upcoming AR devices. Meta’s collaboration with EssilorLuxottica positions its products to be more fashionable and appealing to a larger audience.

Moreover, Meta’s Ray-Bans, which now integrate Meta AI, have gained considerable popularity, raising doubts about Snap’s strategy to compete effectively in a market where Meta’s offerings are expected to be superior in both aesthetics and technology.

While potential tariffs on imports from China may impact pricing dynamics, Meta’s strategic positioning suggests they are likely to benefit more from such developments than Snap.

I may not have a complete understanding of all factors at play, but if I were an investor in Snap, I would seek more clarity regarding the roadmap for its AR initiatives. If the strategy is merely to challenge Meta and hope for favorable outcomes, it might be prudent to reconsider focusing efforts on alternative growth avenues.

Regardless, Snapchat’s expertise in AR effects remains a compelling selling point, evidenced by a 49% year-over-year increase in Lens usage among posted Snaps. This growth underscores the platform’s potential to leverage augmented reality as a key differentiator in the social media space.

Overall, Snapchat’s performance reflects a positive trajectory, bolstered by a strategic focus on acquiring new advertising clients and maximizing revenue opportunities rather than relying solely on user growth. Although Snapchat is expanding its user base, the stagnation in key revenue markets necessitates a shift towards optimizing existing resources.

However, these constraints raise concerns about Snap’s ability to sustain revenue growth if user acquisition slows or reaches a plateau in these regions. Consequently, the company must explore new partnerships and opportunities in Asia and the EU, where potential growth exists, although the EU market remains challenging and unpredictable.

Ultimately, Snap faces ongoing challenges concerning its future direction and strategies to drive market growth. Although improvements in the U.S. market are commendable, the lack of user acquisition poses limitations, and current figures may merely reflect seasonal promotional activities.

As Snap prepares for its Q1 2025 results, there is potential for a different narrative. However, I remain skeptical about its future growth strategies in both AI and AR, particularly given the intense competitive landscape it faces.